TEG Retirement & Advisory Services – Building Health Care Costs into Retirement Planning

Health care planning is a sensitive subject that often takes you and your advisor places you don’t want to go. But given rising expenses, no retirement plan is complete without some kind of provision for health care needs. Here are some guidelines and resources for estimating your needs and expenses.

Health care costs are rapidly emerging as a major expense item both before and during retirement. With lifetime employment a relic of the past and longevity on the rise, it’s more important than ever to estimate how much to save to cover costs in retirement and include those expenses in your financial plan.

Not only are health care costs a huge factor in retirement, but they are also becoming a larger concern for pre-retirees. So the conversation about health care costs should not be confined to the years immediately before and during retirement.

Health concerns and health care costs should be an agenda item at each year’s meeting with your financial advisor — no matter what your age is. There are a number of issues surrounding health care and health care costs to be aware of, including the impact of how you take care of health care costs, what issues you potentially face pre-retirement, what you need to do to prepare for health care costs in retirement, and continuing adjustments you might need to make in your spending and planning during retirement.

Health care status

There is one aspect of health care and health care costs that is controllable amid many that are not: whether you are in good health or not. For many with poor health, discretionary spending on items such as vacations may have to be diverted into health care in retirement, an outcome that is preventable in most cases.

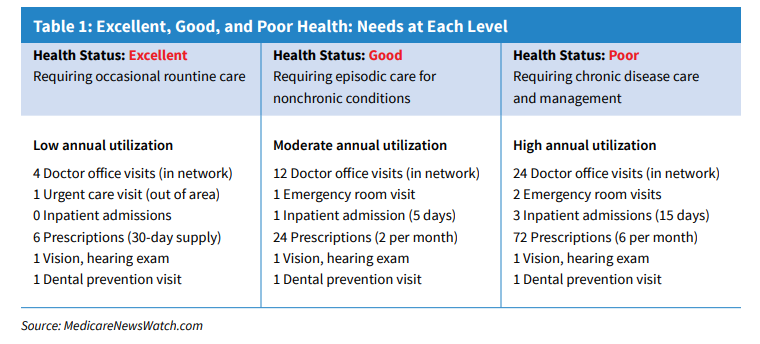

To determine the state of your current health, visit the MedicareNewsWatch.com website. It defines three states of health—excellent, good, or poor—very concretely in terms of number of doctors’ visits per year, number of hospital admissions, and number of prescriptions.

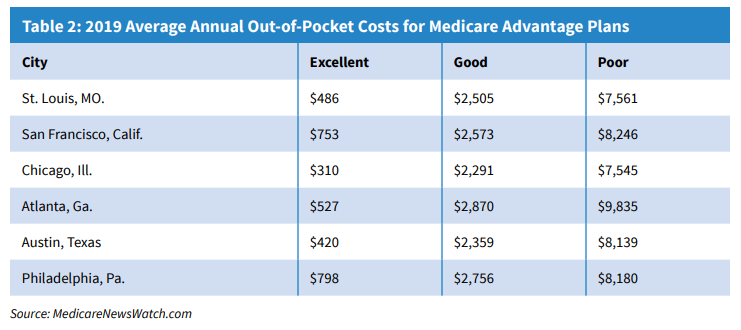

Based on data from the site and your location, you can determine the impact your health status might have on your expenses in retirement. The table below provides an example for residents of several different cities of the average annual out-of-pocket costs for Medicare Advantage plans based on the lowest-cost health plan in the site’s database. These costs include Part D (drug benefit) costs.

For many people in their early 50s, this is enough to motivate them to go home and get on the treadmill. Of course, there are circumstances that you have little control over, such as a cancer diagnosis. But even when disease cannot be avoided, becoming aware of the potential health care costs in retirement can make a difference in how you save and execute your financial plan.

Preparing for retirement

While it’s good to start thinking about retiree health care in your 40s or 50s, discussions should begin in earnest by age 63. Prior to that, it’s difficult to get a handle on the specific costs you are likely to incur.

However, at 63, it’s time to sit down and project actual costs. For couples, those costs are doubled—there are no health care discounts for couples. Topics to be reviewed include Medicare, including premiums and co-pays, out-of-pocket costs for items Medicare doesn’t cover, and costs for unexpected events, like a major health crisis such as cancer.

Many experts recommend computing health care costs going forward with a higher average rate of inflation than other retirement costs – maybe as much as two to four times the Consumer Price Index.

Your 63rd birthday is also a good time to get serious about digging into which specific Medicare plans you will choose. You may even want to enroll in Medicare when you turn 64 and through that year before you turn 65 because it can be a stressful and emotional time. Consider creating a step-by-step calendar of the dates involved in signing up for the various parts of Medicare.

In retirement

The numbers involved in paying for health care costs in retirement are so large that it’s easy to shy away from incorporating those numbers into your retirement plan.

Some experts believe that a 65-year-old couple will need about $280,000 for overall medical expenses in retirement. For instance, Medicare Part B, which covers outpatient care, preventive and ambulance services, and medical equipment, will cost each person about $1,811 annually (that’s a $185 deductible and a year’s worth of $135.50 premiums.) Medical expenses are usually at least an annual $6,500 per person at the start of retirement.

The good news is that this amount is something you can save up front, as well as fund as you go. As you age, your health care costs typically continue to increase beyond even inflation, mostly because you are sicker and likely to require more hospital visits, more medications, and more care in the home or in a nursing home. A large portion of health care costs in retirement occurs in the last few months of life.

Copyright © 2019 by Horsesmouth, LLC. All rights reserved. IMPORTANT NOTICE This reprint is provided exclusively for use by the licensee, including for client education, and is subject to applicable copyright laws. Unauthorized use, reproduction or distribution of this material is a violation of federal law and punishable by civil and criminal penalty. This material is furnished “as is” without warranty of any kind. Its accuracy and completeness is not guaranteed and all warranties expressed or implied are hereby excluded.

All information herein has been prepared solely for informational purposes, and it is not an offer to buy or sell, or a solicitation of an offer to buy or sell any security or instrument or to participate in any particular trading strategy. Securities offered through LPL Financial, member FINRA/ SIPC. Insurance products offered through LPL Financial or its licensed affiliates. Financial Planning offered through Lexco Wealth Management, a registered investment advisor and a separate entity from LPL Financial.

![]()