Are you interested in finance, accountability, and giving back to your community? TEG Federal Credit…

Inflation and Home Prices: What to Know

Published on April 13, 2026

Inflation and home prices are back in focus as rising energy costs pushed inflation higher in March. While this may sound concerning, there are also signs of opportunity, especially for future homebuyers. Here’s a simple breakdown of what’s happening and what it could mean for your finances.

Inflation is Rising, Here’s Why It Matters

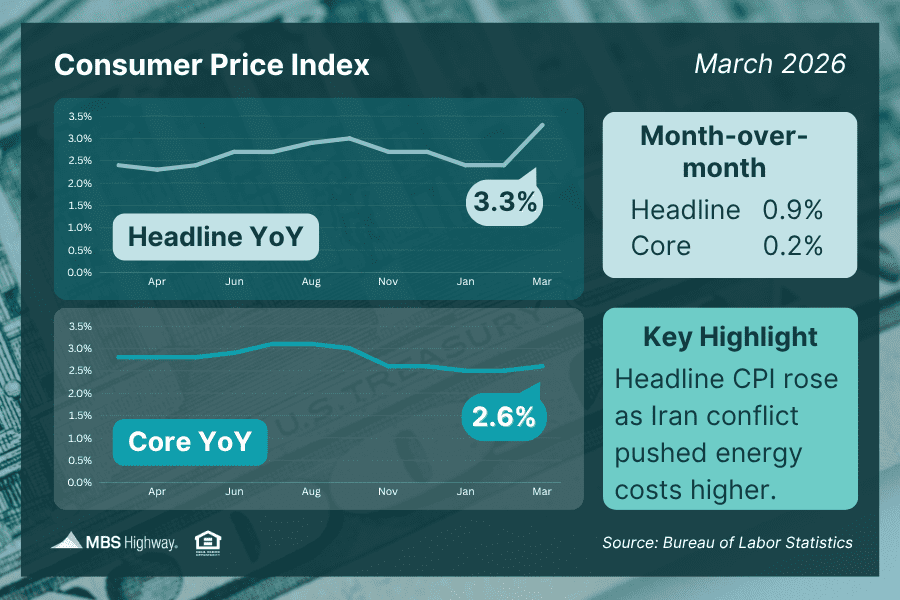

Inflation picked up in March, with overall prices increasing faster than expected. A big reason?! Higher energy costs, including fuel and gasoline.

When energy prices rise, it impacts everyday expenses, from commuting to groceries, making it more expensive to manage your monthly budget.

At the same time, “core inflation” (which excludes food and energy) remained more stable. This tells us that while prices are rising, the increases may not be happening across every category.

What does this mean for interest rates?

The Federal Reserve is keeping a close eye on two key factors:

- Inflation is still higher than their target

- The job market may be starting to slow down

Because of this, the Fed is taking a cautious approach. While rate cuts could happen later this year, nothing is guaranteed yet.

Bottom line: Borrowing costs, including loans and mortgage, may stay elevated in the short term.

Home Prices Continue to Show Strength

While inflation is rising, home prices have remained relatively stable, and are expected to grow.

Recent data shows:

- Home prices were mostly flat month-over-month

- Values increased slightly compared to last year

- Prices are projected to rise around 4-5% over the next year

Why this matters for you

Homeownership continues to be one of the most reliable ways to build long-term wealth.

For example:

A $500,000 home increasing by 5% in value could gain about $25,000 in just one year.

That’s growth that can build over time, especially for buyers who plan to stay in their home long-term.

Bottom line: Even in a higher-rate environment, buying a home can still be a smart financial move.

A Quick Look at the Economy

The broader economy is showing mixed signals:

- Economic growth slowed significantly at the end of 2025

- Unemployment claims increased slightly

- Some workers are turning into a freelance or gig work instead of filing for benefits

- Fewer people are continuing to collect unemployment, but job searches may be taking longer

What this means overall

The economy isn’t declining, but it is cooling.

Bottom line: A slower economy could eventually lead to lower interest rates, but the timing remains uncertain.

The Bottom Line

Rising energy costs are pushing inflation higher, which may keep interest rates elevated for now. However, there are still positive signs, especially in the housing market.

- Inflation is increasing, but not across all categories

- The Fed is proceeding carefully with rate decisions

- Home prices are expected to continue growing

- The economy is slowing, but still stable

For many people, this creates a balanced environment: higher borrowing costs in the short term, but continued long-term opportunities, especially when it comes to homeownership.

Categories: Mortgage & Home Loans

More Recent Posts

Have you received a text message, email, or letter offering hundreds of dollars a week…

Strong Employment Data Continues to Support the Economy Recent labor market reports delivered encouraging news…

Inflation Remains Elevated, But the Economy Continues to Move Forward Inflation and interest rates continue…