Are you interested in finance, accountability, and giving back to your community? TEG Federal Credit…

Fed Holds Rates Steady: What It Means For You

Published on May 5, 2026

The news that the Fed holds rates steady is making headlines—but what does that actually mean for you, your finances, and especially your homebuying plans?

From rising gas prices to steady home appreciation, there’s a lot happening in the economy right now. Let’s break it down in a simple, straightforward way so you know what to expect.

Fed Holds Rates Steady—But There’s More to the Story

The Federal Reserve recently chose to keep its benchmark interest rate unchanged for the third straight meeting.

While this rate doesn’t directly set mortgage rates, it heavily influences borrowing costs across the economy—including loans, credit cards, and mortgages.

What’s the Bottom Line?

Even though the decision was expected, there’s growing disagreement among policymakers. Some want rate cuts soon, while others prefer to stay cautious due to ongoing inflation.

👉 What this means for you:

Mortgage rates may not drop quickly. Instead, expect gradual changes as the economy continues to shift.

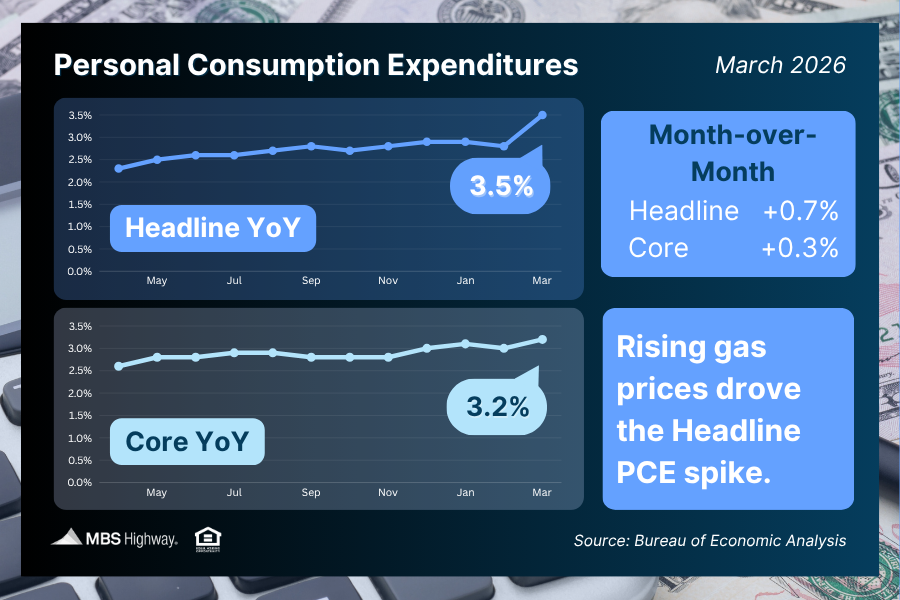

Gas Prices Are Pushing Inflation Higher

Inflation ticked up recently, largely due to rising gas prices.

- Overall inflation rose faster than expected

- Core inflation (excluding food and energy) increased more slowly

What’s the Bottom Line?

Inflation is still above the Federal Reserve’s target, which is one reason rates aren’t being cut yet.

👉 What this means for you:

Higher inflation can keep borrowing costs elevated, impacting everything from car loans to mortgages.

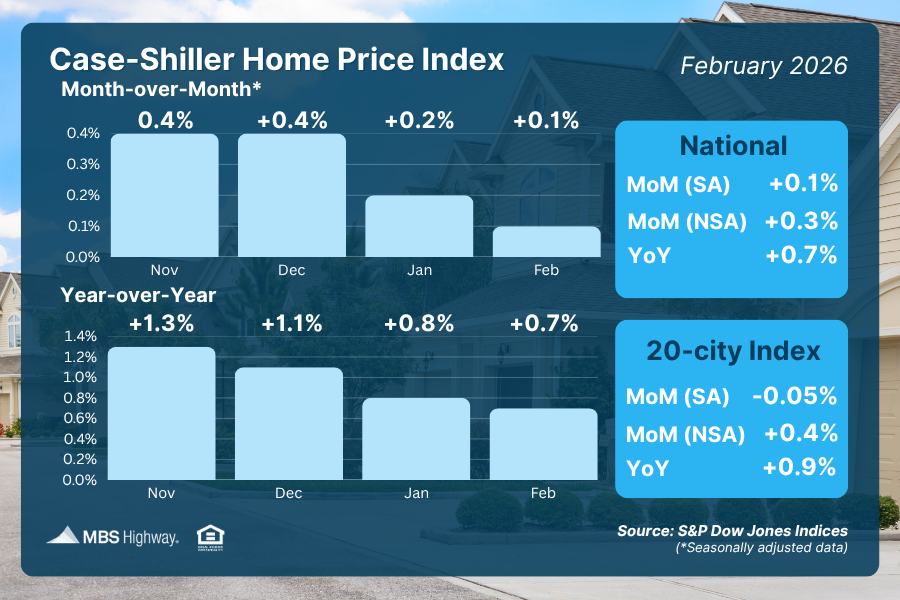

Home Prices Are Still Rising

Home values continue to increase—marking seven straight months of growth.

Even though the pace is modest, it’s steady and meaningful over time.

What’s the Bottom Line?

Homeownership remains a powerful long-term investment.

For example:

A $500,000 home growing at just 3% annually could gain about $15,000 in value in one year.

👉 What this means for you:

Waiting to buy could mean paying more later as home values continue to climb.

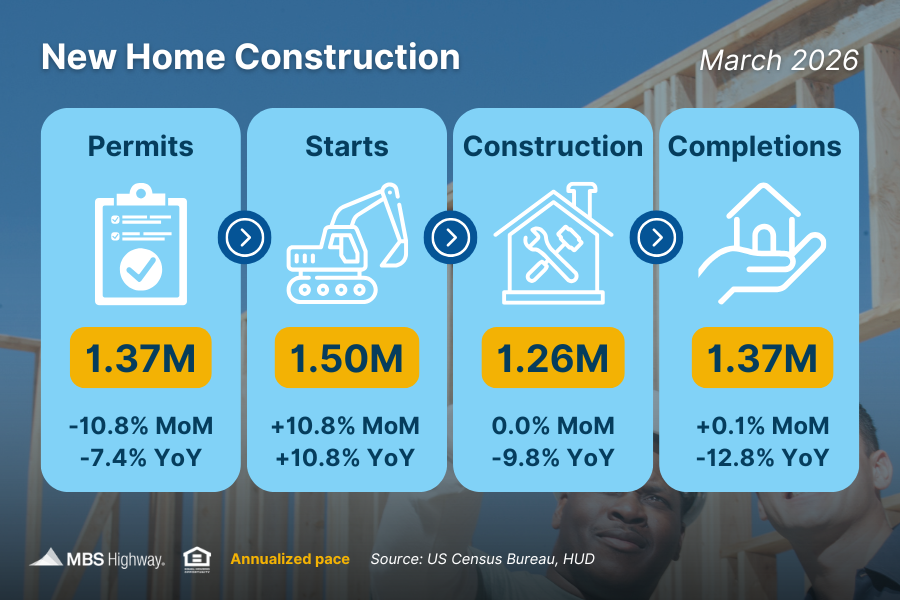

Housing Market Shows Mixed Signals

There’s some good news, and some caution, in new construction data:

- Housing starts increased, meaning more homes are being built

- Building permits declined, signaling possible slower construction ahead

What’s the Bottom Line?

Builders are active, but still cautious due to economic uncertainty.

👉 What this means for you:

Inventory may improve in the short term, but supply could remain tight longer term.

The Economy is Holding Steady

Recent reports show:

- Economic growth rebounded in early 2026

- Unemployment claims remain low

What’s the Bottom Line?

The economy is stable overall, but there are still mixed signals that the Fed is watching closely.

👉 What this means for you:

A steady job market is a positive sign if you’re considering buying a home or refinancing.

How This Impacts Mortgage Rates

Mortgage rates don’t move exactly with the Fed, but they are influenced by:

- Inflation trends

- Economic growth

- Market expectations

Right now, the combination of steady rates and persistent inflation suggests mortgage rates may stay somewhat elevated in the near term.

How TEG Federal Credit Union Can Help

Whether you’re buying your first home or thinking about refinancing, having the right guidance matters.

At TEG Federal Credit Union, our mortgage team is here to help you:

- Understand today’s rate environment

- Explore loan options that fit your budget

- Make confident, informed decisions

We’re committed to helping you navigate changing market conditions with clarity and confidence.

The Bottom Line

- The Fed is holding rates steady, but future decisions are uncertain

- Inflation remains elevated, largely due to gas prices

- Home values are still rising, reinforcing long-term benefits of buying

- Housing supply is improving, but cautiously

- Mortgage rates may remain higher in the short term

👉 Smart takeaway:

If you’re thinking about buying a home, focusing on long-term value, not short-term rate changes, can help you make a more confident decision.

Categories: Mortgage & Home Loans

More Recent Posts

Have you received a text message, email, or letter offering hundreds of dollars a week…

Strong Employment Data Continues to Support the Economy Recent labor market reports delivered encouraging news…

Inflation Remains Elevated, But the Economy Continues to Move Forward Inflation and interest rates continue…