Are you interested in finance, accountability, and giving back to your community? TEG Federal Credit…

Inflation Cools as Expected While Housing Contracts Stall

Published on January 27, 2026

Market Snapshot

Here’s our latest inflation and housing market update: Recent economic data delivered a mix of encouraging inflation news and softer housing activity. The Federal Reserve’s preferred inflation measure matched expectations, while signed home contracts slowed as winter weather and holiday disruptions weighed on buyer activity.

Here are the key highlights this week:

- Inflation data showed continued progress

- Pending home sales declined in December

- Economic growth surged in the third quarter

- Jobless claims point to low layoffs but slower hiring

Let’s break it down.

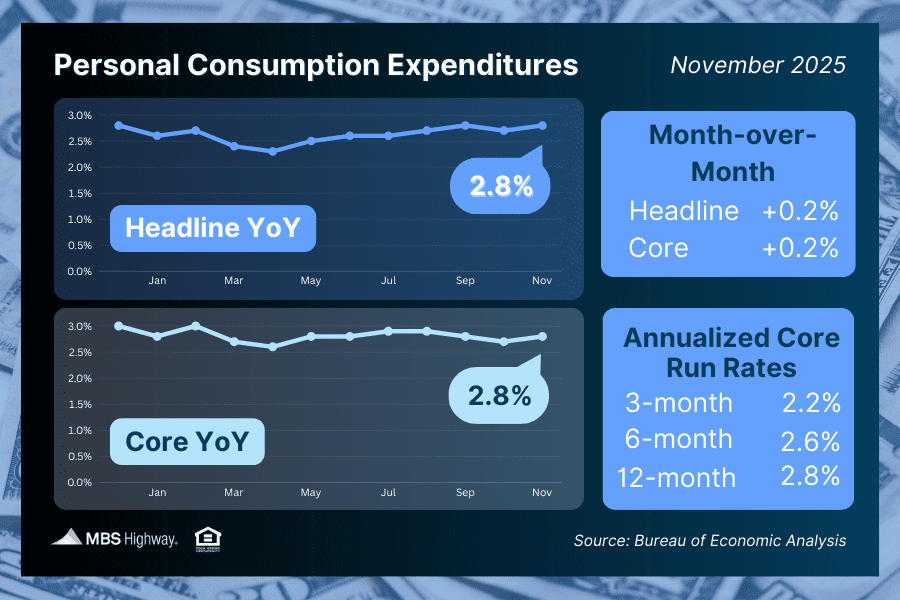

PCE Inflation Data Offers Encouraging Signs

The government released the delayed Personal Consumption Expenditures (PCE) reports for October and November — the Federal Reserve’s preferred inflation gauge.

What we saw:

- Headline inflation: +0.2% in both months

- Core inflation (excluding food and energy): +0.2%

- Annual inflation rate: 2.8%

These results came in exactly as economists expected.

Why this matters

The Fed continues walking a tightrope between:

- Persistent inflation pressures, which argue against rapid rate cuts

- Signs of a cooling labor market, which increase pressure to ease policy

Last fall, the Fed cut its benchmark Federal Funds Rate by 25 basis points three times. While this rate does not directly control mortgage rates, it strongly influences borrowing costs throughout the economy.

Fed Chair Jerome Powell has emphasized that there is “no risk-free path” forward — meaning future decisions will depend heavily on incoming inflation and employment data.

The encouraging part

Monthly inflation readings remained relatively tame:

- October: 0.21%

- November: 0.16%

If inflation remains subdued early this year, progress toward the Fed’s 2% target could accelerate as higher readings from early 2025 roll out of the annual calculation.

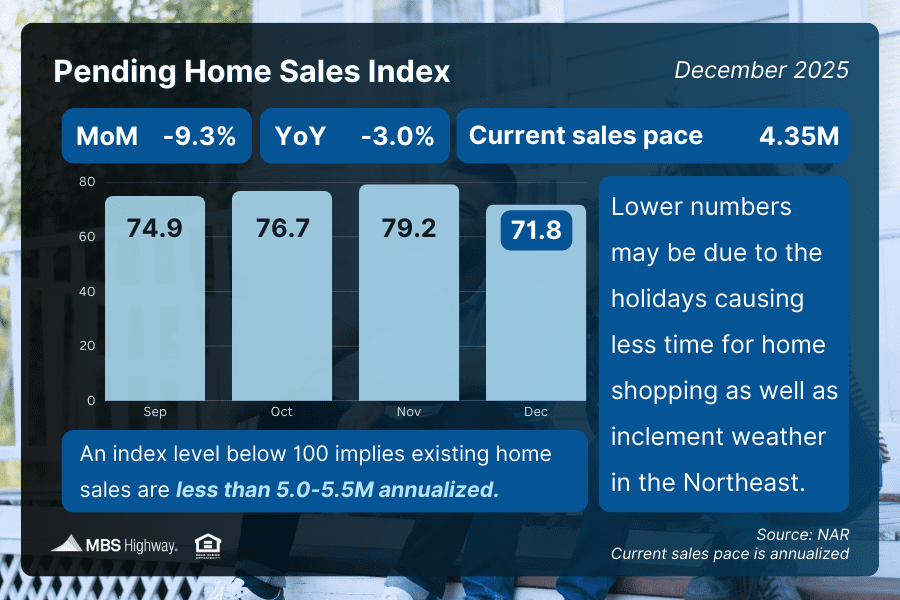

Pending Home Sales Slide

According to the National Association of

REALTORS ® (NAR):

- Pending home sales fell 9.3% from November to December

- Signed contracts were down 3% year over year

This decline followed four consecutive months of gains.

What’s behind the drop?

NAR Chief Economist Lawrence Yun noted that December data is often difficult to interpret due to:

- Holiday schedules

- Vacation time

- Winter weather disruptions

These factors can temporarily distort buyer activity.

Inventory remains the bigger issue

While home closings increased in December, new listings failed to keep pace, pushing inventory even lower.

- Homes for sale: 1.18 million nationwide

- Matching the lowest inventory level of 2025

With fewer options available, many buyer may have delayed or paused their home search.

Q3 GDP Surges to Fastest Pace Since 2023

After delays caused by the government shutdown, the final estimate for Q3 2025 GDP was released.

The numbers:

- Economic growth: 4.4% annualized

- Previous estimate: 4.3%

- Fastest quarterly growth since Q3 2023

This marks a significant acceleration from:

- 3.8% growth in Q2

- 0.6% contraction in Q1

For the first nine months of the year, the U.S. economy is averaging 2.5% growth.

What drove the increase?

Several factors contributed:

- Strong consumer spending

- A surge in electric vehicle purchases ahead of the EV tax credit expiration

- Increased business investment

- Higher government spending

- Stronger exports

- A decline in imports, which boosts GDP calculations

Overall, the data reflects solid — though uneven — economic momentum.

Jobless Claims Show Low Layoffs, Slower Hiring

The latest labor market data continues to show resilience.

- Initial jobless claims: 200,000 (up to 1,000)

- Continuing claims: 1.849 million (down 26,000)

What this tells us

- Layoffs remain historically low

- The rise of the gig economy is changing unemployment trends

Many displaced workers are choosing contract or app-based work rather than filing for unemployment benefits, which often fall short of covering living and housing expenses.

However, continuing claims remain elevated, indicating that job seekers are taking longer to find permanent positions, signaling some softening beneath the surface.

The Bottom Line

- Inflation continues to cool gradually and remains on track with expectations.

- The Federal Reserve remains cautious, balancing inflation progress with labor market conditions.

- Housing contract activity slowed in December, likely influenced by seasonal factors and tight inventory.

- Economic growth surprised to the upside, while the labor market shows low layoffs but slower hiring momentum.

As always, mortgage rates will continue responding to inflation trends, economic data, and market expectations — not just Fed policy moves.

Staying informed and prepared remains key as markets navigate the months ahead.

Categories: Education, Mortgage & Home Loans

Tags: housing market, tegfcu

More Recent Posts

TEG Federal Credit Union will award three $1,000.00 scholarships to graduating high school seniors who…

Following last fall’s government shutdown, several key economic reports were released at once—including updates on…

What the January Economic Data Is Telling Us At first glance, January’s economic reports delivered…

It’s Friday the 13th. Black cats.Broken mirrors.Walking under ladders. Some people swear it’s unlucky. Others…