Are you interested in finance, accountability, and giving back to your community? TEG Federal Credit…

Fed Holds Rates Steady, Trump Names Chair Pick

Published on February 2, 2026

President Trump announced his pick for the next Federal Reserve chair, the Fed hit pause on rate cuts at its first meeting of the year, and new housing data showed renewed national strength in home prices. Below are the key takeaways — and what they could mean for mortgage rates and the housing market.

Trump Taps Kevin Warsh for Fed Chair

President Trump revealed plans to nominate Kevin Warsh as the next chair of the Federal Reserve. Warsh previously served on the Fed’s Board of Governors from 2006 to 2011 and would replace current Chair Jerome Powell when his term ends in May, pending Senate confirmation.

Warsh has long been viewed as an inflation hawk, having previously warned that overly accommodative monetary policy could fuel rising prices. More recently, however, he has suggested the Fed should move more quickly to cut interest rates — a stance that aligns more closely with the administration’s criticism of the Fed’s handling of inflation over the past several years.

Bottom line: Leadership changes at the Fed can influence market expectations, but any real policy shifts would take time and depend heavily on future economic data.

Fed Pauses Rate Cuts, Two Officials Dissent

As expected, the Federal Reserve held the Federal Funds Rate steady at 3.50%-3.75%, following three consecutive quarter-point cutes late last year. While this rate doesn’t directly set mortgage rates, it plays a major role in shaping overall borrowing costs throughout the economy.

The decision, however, was not unanimous. Governors Stephen Miran and Christopher Waller voted in favor of another rate cut, highlighting the ongoing tension within the Fed.

The central challenge remains balancing:

- Inflation that is still running above the Fed’s target, and

- Signs of a cooling labor market that could justify lower rates

Notably, the Fed also removed language from its statement that previously reference rising downside risks to employment. Governor Waller strongly disagreed with this change, warning that meaningful labor market deterioration remains a real risk.

Markets currently expect rates to remain on hold for the next couple of Fed meetings, though that outlook could shift quickly if inflation of employment data surprises.

Bottom line: The Fed is cautious, divided, and highly data-dependent — meaning rate volatility could continue.

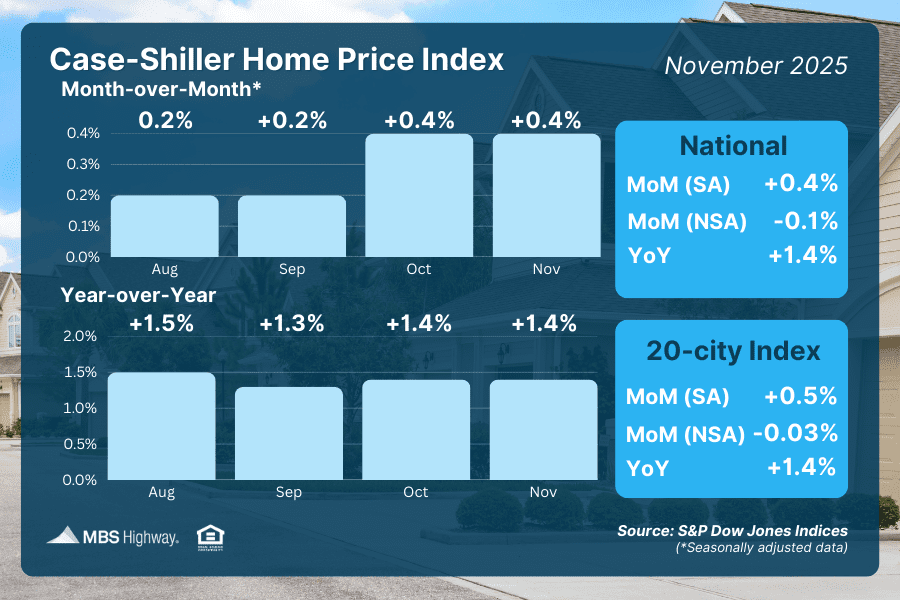

Buyer Demand Supports Home Prices

Recent home price data showed resilience, even amid higher interest rates.

The Case-Shiller Home Price Index recorded a modest 0.1% decline from October to November before seasonal adjustments. After adjusting for typical seasonal trends, prices actually rose 0.4%. On a year-over-year basis, national home prices are still 1.4% higher than last year.

The FHFA Home Price Index, which tracks homes financed with conventional mortgages, showed even stronger results:

- Prices rose 0.6% month over month, and

- Were 1.9% higher than a year ago

What’s driving this? Mortgage rates eased slightly in recent months, helping bring buyers back into the market. At the same time, builders have scaled back construction, and new housing supply cannot increase quickly due to permitting and construction timelines.

Bottom line: If mortgage rates continue to trend lower, renewed buyer demand could place additional upward pressure on home prices.

Key Labor and Inflation Updates

On the labor front, initial jobless claims fell slightly to 209,000, while continuing claims declined to 1.827 million. Even so, continuing claims remain elevated compared to earlier periods, suggesting some workers are experiencing longer job searches or shifting toward gig and contract work instead of filing for unemployment.

Inflation data came in hotter than expected:

- The Producer Price Index (PPI) rose 0.5% month over month and 3.0% year over year

- Core PPI, which excludes food and energy, increased 0.7% for the month and 3.3% annually

Much of the increase was concentrated in machinery and equipment wholesaling margins, suggesting inflation pressures were relatively narrow rather than broad-based.

Bottom line: Inflation remains sticky, but not all sectors are seeing the same level of price pressure — something the Fed will be watching closely.

The Takeaway

The Fed is signaling patience, housing demand is proving resilient, and inflation remains the key wildcard. For borrowers, this means mortgage rates may stay volatile in the near term — but improving demand and easing rates could support housing activity as the year progresses.

If you’re thinking about buying, refinancing, or just keeping an eye on market conditions, staying informed can help you make confident financial decisions.

Categories: Education, Mortgage & Home Loans

More Recent Posts

TEG Federal Credit Union will award three $1,000.00 scholarships to graduating high school seniors who…

Be honest with yourself. Have you started looking at homes online yet? Scrolling through real…

Our Power, Our Planet 🌎 This Earth Day, we’re reminded that small choices make a…

A Closer Look at Today’s Economy In this blog, we’ll share a jobs report and…