Are you interested in finance, accountability, and giving back to your community? TEG Federal Credit…

What Today’s Economic Data Means for Homebuyers

Published on February 23, 2026

Following last fall’s government shutdown, several key economic reports were released at once—including updates on inflation, housing activity, GDP growth, and unemployment. Together, these reports offer a clearer picture of where the economy stands and what may lie ahead for interest rates, housing supply, and affordability.

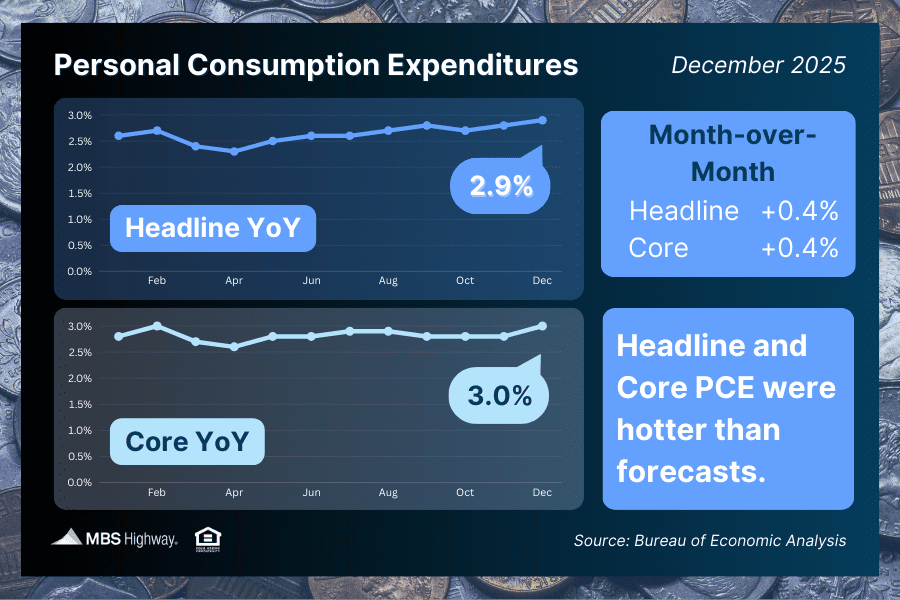

Inflation Came in Hotter Than Expected

The Federal Reserve’s preferred inflation measure, Personal Consumption Expenditures (PCE), showed prices rose more than economists expected in December.

- Headline inflation: Up 0.4% for the month, bringing the annual rate to 2.9%

- Core inflation (excluding food and energy): Also up 0.4% with an annual rate of 3.0%

One surprising contributor? Higher costs for video streaming services, which jumped nearly 20% in a single month, adding to the overall price pressures.

Why this matters

Inflation remains above the Fed’s long-term 2% goal. That makes policymakers cautious about cutting interest rates too quickly—even as other parts of the economy show signs of cooling.

The good news: annual inflation numbers could improve in the months ahead as higher readings from early 2025 drop out of the 12-month calculation, assuming monthly inflation stays moderate.

Bottom line: Inflation is easing, but not fast enough yet to guarantee near-term rate cuts.

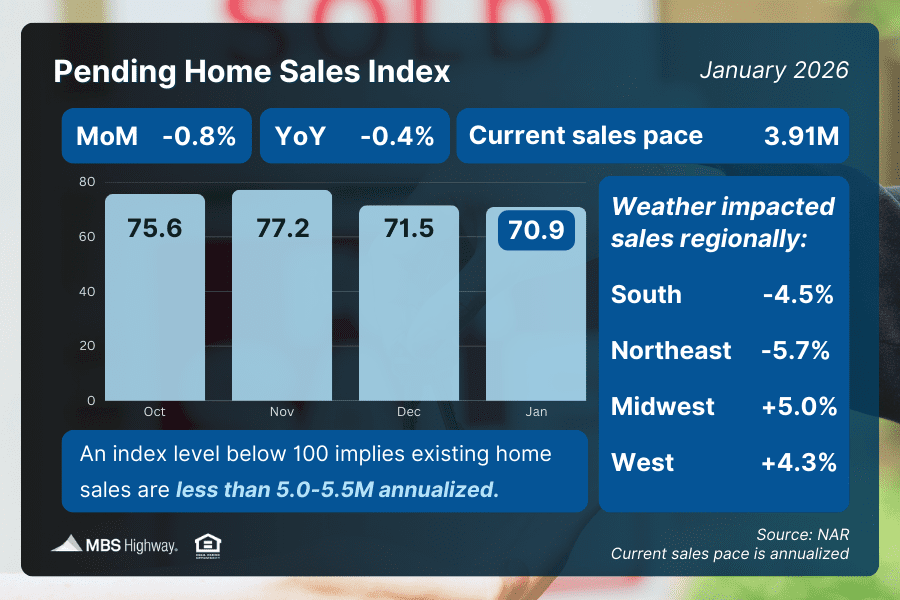

Winter Weather Slowed Homebuying Activity

Pending Home Sales, which track signed contracts on existing homes, fell 0.8% from December to January and were 0.4% lower than a year ago.

Severe winter storms likely played a role, particularly in the South and Northeast. Meanwhile, contract activity improved in the West and Midwest.

It’s worth noting that new-home contract activity has been much stronger, reaching its highest levels in nearly four years late last fall.

Why this matters

Lower mortgage rates could bring hundreds of thousands of additional buyers into the market this year. However, if housing inventory doesn’t increase alongside that demand, home prices could face renewed upward pressure.

Bottom line: Buyer interest is there—but limited supply remains a key challenge.

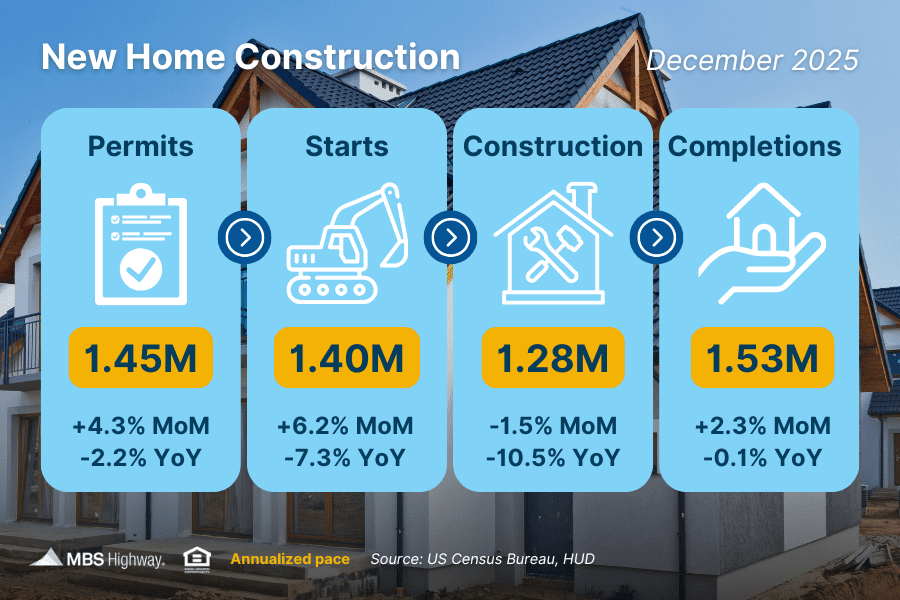

Home Construction Is Improving—Slowly

New home construction showed modest improvement at the end of the year:

- Housing Starts: Up 6.2% month over month to an annual pace of 1.404 million, though still 7.3% lower than last year

- Building Permits: Up 4.3% month over month, signaling potential future construction

Despite the improvement, builder confidence remains low. The Housing Market Index stayed well below the 50 mark, meaning more builders view conditions as poor than good.

Builders continue to cite:

- Affordability concerns

- Higher construction and labor costs

- Ongoing supply chain pressures

Lower mortgage rates have helped, but new supply takes time—from permits to completed homes.

Bottom line: Construction is moving in the right direction, but not fast enough to quickly solve the housing shortage.

Quick Take: GDP Growth and Unemployment

- GDP: The first estimate of Q4 2025 growth showed the economy expanded at an annualized rate of 1.4%, down sharply from 4.4% in Q3. Reduced government spending during the shutdown was a major factor.

- Unemployment claims: Initial jobless claims feel to 206,000, though holiday timing may have influenced the drop. Continuing claims rose to 1.87 million, suggesting some workers are taking longer to find new jobs.

Why this matters

Slower economic growth combined with a cooling labor market could eventually increase pressure on the Fed to ease rates—but inflation still has the final say.

The Bottom Line

- Inflation is improving but remains above target

- Housing demand is strong, but supply is still limited

- Construction is increasing slowly, not rapidly

- Economic growth is cooling, while the job market shows mixed signals

For homebuyers and homeowners, this environment reinforces the importance of watching rates closely, understanding affordability, and being prepared when opportunities arise.

Categories: Mortgage & Home Loans

More Recent Posts

TEG Federal Credit Union will award three $1,000.00 scholarships to graduating high school seniors who…

Be honest with yourself. Have you started looking at homes online yet? Scrolling through real…

Our Power, Our Planet 🌎 This Earth Day, we’re reminded that small choices make a…

A Closer Look at Today’s Economy In this blog, we’ll share a jobs report and…