Blog

Spring Clean Your Finances

Personal loans can be a game-changer in your spring plans. Whether you have a project in mind or want to consolidate your high-interest credit card bills into one lower, fixed-rate payment, it’s a great time to lock in your rate, and start saving today! How […]

View moreNavigating the Volatile Housing Market

Should You Buy or Sell Now? The housing market is always changing, and in recent years, it has become more unpredictable. This has left many potential buyers and sellers wondering whether it is the right time to move. Factors Contributing to Housing Market Volatility Several […]

View moreHow life events can change your housing needs.

Are you contemplating buying a home this year? Taking such a significant leap forward is a crucial milestone. Life-changing events such as marriage, divorce, job opportunities, or just the desire for a better lifestyle often spur this decision. We’re aware that today’s economic climate and […]

View moreWhy it’s a good time to earn more with a 6-Month Certificate

Trying to maximize your savings? That’s smart! But let’s face it, finding the right place to invest that hard-earned cash can be a bit tricky. Why? Well, the financial world can be like a roller coaster – unpredictable and rapidly changing. But don’t worry, we’re […]

View more2024 TEG Annual Meeting

YOU are the reason we love what we do—improving lives. Helping people get to a better place financially. Member Focused. Member Driven. Together Everyone Grows. Over the past five decades, TEG has grown to serve over 37,000 members and is approaching $420 million in assets. […]

View moreWhy the Holidays are a Good Time to Consolidate Your Debts

During the holiday season, you’re likely making a list and checking it twice. But between gifts, travel, and festive celebrations, it’s easy to lose sight of holiday spending and your financial goals. This year, why not add “consolidate my debts” to your wish list? The […]

View moreThanksgiving Dinner Tips

10 Easy Suggestions for a Stress-Free Thanksgiving Dinner Hosting a stress-free Thanksgiving meal can be emotionally overwhelming and break your budget, but it doesn’t have to. Follow these tips for Thanksgiving dinner to enjoy a calm and budget-friendly holiday celebration. Plan Ahead Don’t wait until […]

View moreFree Community Shred Events

Shred it. Don't regret it. Fraud and identity theft have become an epidemic in our communities, and to raise awareness and promote prevention, we host these FREE community service shred events for you, our members. TEGFCU hosts these events to provide community residents and businesses [...] View more

In a High Mortgage Rate Environment – What Are Your Options to Buy a Home?

Buying a home is one of the most significant investments you’ll make. Low mortgage rates have made it easier for people to afford their dream homes over the last dozen years. In 2023, home mortgage rates have been soaring, causing problems for people who want […]

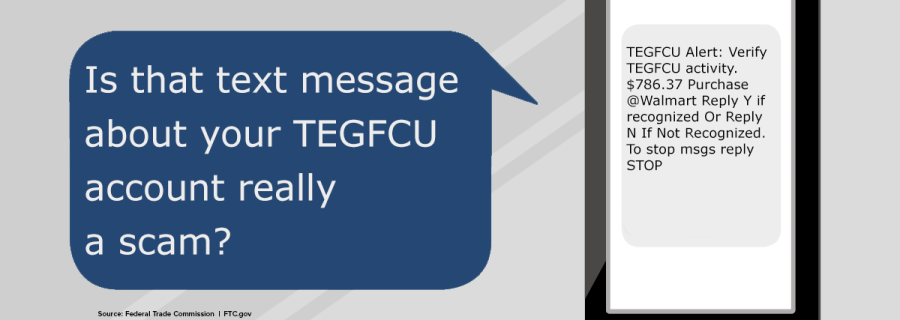

View moreBeware of Text Message Scams

The Federal Trade Commission (FTC) is warning consumers about text message scams. The FTC found that fake bank fraud alerts were the most common text message scam reported in their study. The study also revealed that many popular financial text scams pretend to be from […]

View moreDon’t Be Tricked By Social Engineering Scams

Social Engineering Scams have increased over the past few years, with incidents increasing alarmingly. Social Engineering is a term that refers to using psychological techniques to manipulate someone. This exploitation can lead to revealing sensitive information, like passwords, bank account numbers, and debit card pins. [...] View more

Why Should I Shred My Documents?

That question can be answered in two words: Identity Theft. The number of security issues continues to rise and is a critical concern for businesses and individuals. Securing private information and disposing of it safely has never been more important. Financial documents may contain a [...] View more

Know the Signs of a Scam

How Do I Know If I’m Talking to a Scammer? Know the signs of a scam. The internet has made communicating with others much easier, but it also makes it easier for scammers to find new victims. Scammers are constantly looking for people to take […]

View moreScam Alert – Members Beware – Telephone and Text Scams

Please be aware of a phishing telephone scam that some credit unions across the country are reporting more frequently. Members are receiving phone calls from fraudsters posing as a credit union employee, who tell them that their account has been compromised or that their credit/debit […]

View moreWhat is an Adjustable-Rate Mortgage?

What do I need to know about Adjustable-Rate Mortgages? An adjustable-rate mortgage, or ARM, is a home loan with an interest rate that can change periodically. This means that your monthly mortgage payment could go up or down over the life of your loan. ARMs […]

View moreBeware of Online Quiz Scams

Online quizzes are a fun way to pass the time and test your knowledge, but they can also be a way for scammers to steal your personal information. In recent years, online quiz scams have become more prevalent, posing a risk to anyone who takes [...] View more

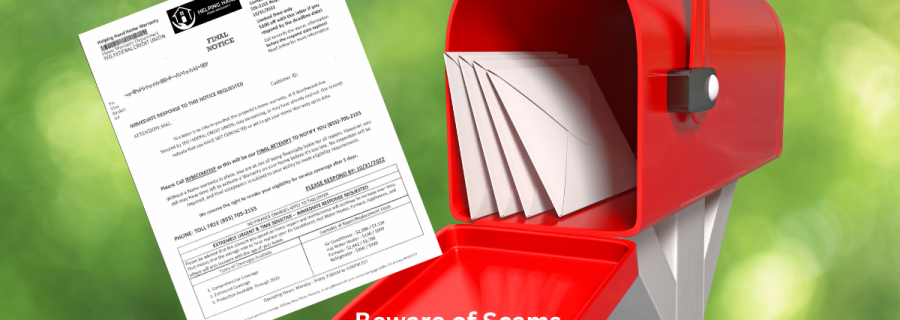

Home Warranty Scams

Home warranty scams are rising. with millions of dollars lost to fraudsters each year. These scams can take many forms, but they all share one common goal: stealing your money. Scammers often pretend to be from companies you know and trust. For example, TEG Federal […]

View moreHow to Use Zelle to Safely Send Money

Zelle® is a fast, safe, and easy way to send and receive money with people you trust, like your babysitter, coworkers, fellow PTA mom, or your son's soccer coach. Whether you just enrolled with Zelle® or have been an active user for a while, there [...] View more

Postal Mail Theft

If you live in Hudson Valley, it’s time to get on the defensive regarding mail theft. With rising reports of statements, packages, letters, and other important documents going unchecked due to a significant increase in mail thefts across the state, this is not something NY […]

View moreTEGFCU eStatements

Fast. Secure. Convenient. Always Available. Your bank statement is a vital tool for keeping track of your withdrawals and deposits, but more importantly, it also helps you become aware of suspicious activity and possible fraud. Fast – Avoid USPS postal shortcomings, delays, and lost or […]

View moreAnnual Meeting 2023

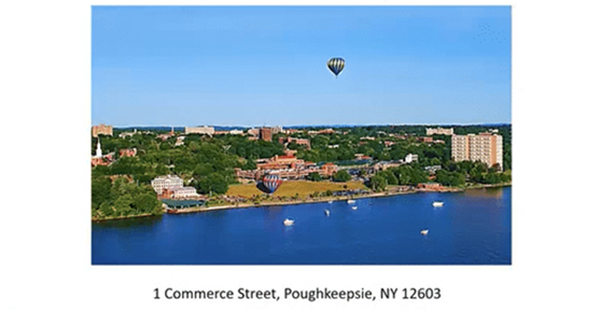

This year’s 54th Annual Meeting was held: March 30, 2023, 5:30 PM 1 Commerce Street, Poughkeepsie, NY, 12603 Each year, TEG Federal Credit Union hosts an Annual Meeting. Our Annual Meeting is a unique opportunity for credit union members to hear about our financial health […]

View moreTEG 2023 Scholarships

Student Scholarships Available We’re ready to support the future generations of our communities. Our scholarship program is an investment in our future and yours. With a solid education, we can all make a difference. TEG Federal Credit Union will award three $1,000.00 scholarships to graduating […]

View moreKeep Yourself Safe from Scams and Fraud

Scams targeting people often play on their trust. We want to empower you to spot the latest scams and know a fraud when you see it. We are seeing an increase in phishing telephone scams involving fraudsters posing as members of a technology department, fraud [...] View more

Renovation Loan

The national trend of homebuyers seeking out properties in need of renovations has established a firm foothold in the Hudson Valley, where low inventory and a critically-low inventory of turnkey houses, have repositioned the market. As a result of these shifting sands, many homebuyers are […]

View more

Debt Consolidation Loan

DEBT CONSOLIDATION LOANWhy Choose TEGFCU? Managing your day-to-day finances can be overwhelming. Managing Debt can leave you gasping for air. But always remember, debt is a part of life, and not all debt is bad debt. Loans that finance the purchase of a new car [...] View more

Auto Lease Buyout: Is it Right for You?

It all starts with an auto lease buyout. Simply put, this involves you buying your car when your lease ends, instead of turning it in, beginning a new lease and getting a different car. A car lease buyout is essentially a used car loan – only this time, you’ve already been driving the vehicle for the past few years.

View moreCredit Builder Loans: Personal Loans to Build Credit

Having a good credit score is critical in the age we live in. Having a low score—or no credit history—can hold you back in life. The good news is that you don’t have to live with a low credit score forever. You can use a […]

View more

The Pros and Cons of Using a Personal Loan to Pay Off Credit Card Debt

Buying things with credit cards is quick and easy—just swipe your card and go. But for many, the ease of making purchases causes their balances to grow to unmanageable levels. If you have one or more high-interest credit cards, a personal loan can be used […]

View more

What is APR and How Does it Affect Your Mortgage?

The annual percentage rate (APR) is a term you’re likely to encounter while reviewing your mortgage options. Thankfully, it’s not difficult to understand—but what is APR exactly? Knowing how the APR works can help compare different loans to help you get the best deal possible. […]

View moreRefinancing a HELOC or Home Equity Loan

If you have either a home equity line of credit (HELOC) or a home equity loan, you may have considered refinancing to get more favorable terms or to save money on interest. Before you refinance, however, there are some important things to consider to make […]

View moreHELOC & Home Equity Loan Tax Deductions

There are many perks to being a homeowner. When you buy a home, for example, the down payment and monthly mortgage payments you make help to grow your equity. Many people take advantage of their home equity by taking out either a home equity line […]

View morePersonal Loan FAQs

Personal loans are among the most common financing options for borrowers. They are highly flexible, relatively easy to obtain, and the interest rates are often lower than other borrowing options, such as credit cards. If you are considering one of these loans, the following are […]

View moreWhat Is a Debt-to-Income Ratio?

If you are thinking about applying for a loan, you may have encountered the term debt-to-income (DTI) ratio while researching your options. When considering applicants for a loan, lenders evaluate this ratio to make sure borrowers don’t have too much debt. Understanding the DTI ratio […]

View morePreparing Your Finances for Interest Rate Hikes

Although interest rates have been very low for a while, they are now rising. To cool the high level of inflation we are experiencing, the Federal Reserve is raising interest rates for the first time since 2018. During the uncertain economic times we are now […]

View moreRising Home Prices and Your Home’s Equity

In just the past two years, home prices all across the nation have increased significantly. If you’ve been wondering what’s going on, the following overview can help you understand why prices are rising and how they affect your home’s equity. Why Are Home Prices Rising […]

View moreHELOC vs. Home Equity Loan When Interest Rates Rise

Many people tap into their home’s equity with either a home equity loan or a home equity line of credit (HELOC). They may use the money they borrow for a home improvement project, to buy new appliances, or for something else. A question that borrowers […]

View moreHow Do Home Equity Loans Work?

A common way that many homeowners borrow money is with a home equity loan. The money you borrow can be used for many different purposes, and the interest rates are usually lower than other borrowing options, like personal loans. The following overview can help you […]

View more

Guide to Home Equity Lines of Credit (HELOCs)

If you’ve built up some equity in your home, you might be thinking about tapping into the cash to fund renovations and anything else you have on your plate. You might also be wondering how a home equity line of credit works. A home equity […]

View moreSign up for eStatements & be entered to win a $100 Adam’s Gift Card

Sign up for e-Statements and get entered to win one of three $100 Adams Fairacre Farms Gift Cards! We at TEG Federal Credit Union don’t want you to get e-Statements because it’s green. Saving trees and time is a great reason for you to want […]

View moreRising Interest Rates Make Personal Loans a Smart Choice

You’ve probably heard it on the news – the Federal Reserve will raise interest rates this year to help slow inflation. According to many economists, we could see up to six or seven rate hikes in 2022. But what does this mean for you? Will […]

View moreBuying a Fixer-Upper in Hudson Valley, NY

Visiting the Hudson Valley should come with a warning – once you’ve experienced it, you will probably fall in love with it. Whether it’s the spectacular fall foliage, outdoor recreational adventures, breathtaking vistas, historic locations, or something else, each year many people are taken by […]

View more

Payday Loans vs. Personal Loans [What You Need to Know]

When many find themselves in financial binds and need quick cash, they often turn to payday loans. These loans are quick and easy to obtain, and the funds are usually available the same day you apply. Although payday loans are convenient, they have some important […]

View more4 Types of Personal Loans

A personal loan is a great choice if you need to borrow some money to pay for a home repair, buy a new appliance, or consolidate high-interest credit card debt. Qualifying is relatively easy, and there are few or no restrictions on what you can [...] View more

How Consolidating Debt Can Improve Your Credit Score

Debt consolidation is a popular strategy that many use to combine several high-interest debts into a new loan with a much lower interest rate. In addition to helping you save money on interest, debt consolidation can also make your debt easier to manage. Instead of [...] View more